Housing Momentum Continues – Strong Q1 Highlights Need for Continued Acquisition and Lot Development

By: Aaron Mendenhall, Chapman Lindsey Commercial Real Estate Services

By: Aaron Mendenhall, Chapman Lindsey Commercial Real Estate Services

TUCSON, Arizona — At the end of 2016 we were excited about attaining 2,699 permits and 1,904 single family house starts for the year. When compared to historical averages of 4,000 to 5,000 permits per year, these numbers seem low. However, it highlights the duration and severity of the recession in Tucson. After bumping around the bottom with around 2,000 permits for several years, a jump to 2,700 permits was a welcome change (a 24% increase from 2015). Last year we had several significant job announcements which, among other things, seemed to improve everyone’s outlook on the Tucson economy and market strength.

So far in 2017 market optimism has continued as permits surged even higher. We started out the year with 241 permits in January, increased to 254 permits in February and finished March with 299 permits. Permit counts have increased month over month since November. The 794 permits for the quarter is a 27.9% increase over the first quarter in 2016 and a 19% increase from the fourth quarter 2016. Increased permits and house starts means reduced lot inventories. Builders have been cautiously optimistic about the strength of the housing market and have been working hard to fill their pipelines with lots. As existing finished lots are pretty much non-existent in the market, builders have been purchasing both raw land and platted lot subdivisions for the past several years. The rate of new lot development has been increasing and just last year more new lots were developed and introduced than were built upon. These new lots are needed, particularly as the market continues to improve.

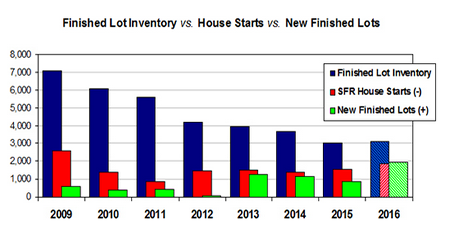

For a historical perspective, single family finished lot inventories were at 10,179 lots at the end of the first quarter in 2008 as the recession was hitting. Builders and developers pulled back from introducing new lots and focused on existing inventories. Finished lot inventories dropped rapidly without replacement lots being introduced to the market. Within a five-year span builders burned through over 6,000 lots and the inventory fell to 3,958 lots by the end of the first quarter of 2013.

Luckily builders and developers recognized the need for new lots as existing lot inventories were picked through and remaining lots were in less desirable locations. They began purchasing platted lots in 2012 and by 2013 these lots started entering the market. The rate of lot inventory reduction began to decline but there were still lot deficits every year. Finished lot inventories bottomed out at 3,013 in the fourth quarter 2015 but stabilized in 2016 as new lot inventory finally exceeded what was being built. At the end of Q1 2017 there were 3,118 finished lots.

As mentioned before, with the improving market and increased permit activity there is even more pressure on builders and developers to continue to introduce new lots to the market to maintain positive lot inventories. The builders’ pipeline management is looking out several years, but they have to walk the fine line of having enough lot inventory to sustain and grow their position without over exposing themselves in the event of a slowdown. The effects of the Great Recession are still in the back of everyone’s minds.

Fortunately, there are several new platted communities that will be coming to market soon that will help alleviate some of the builders’ needs for additional lot inventory in strong locations. We are working with Red Point Development to bring out several new single family communities in the Northwest submarket later this summer, primarily along the Thornydale and Twin Peaks corridors. Combined, these communities will introduce over 670 lots.

DeAnza, located on Hardy Road just north of Cortaro Farms Road, will introduce 251 lots in a coved layout mixing 45’ and 55’ lots.

DeAnza, located on Hardy Road just north of Cortaro Farms Road, will introduce 251 lots in a coved layout mixing 45’ and 55’ lots.

The Hardy & Thornydale property is located on approximately 30 acres. It will have 84 lots with average lot sizes of 55’x115’.

The Thornydale & Magee property is located on the Northwest corner and is comprised of approximately 17.7 acres. The property will yield 36 lots with average lot sizes of 55’x120’.

The Thornydale & Linda Vista property is located across from the Mountain View High School on the Southeast corner. The property is approximately 18 acres with 36 lots. The average lot sizes will be 55’x115’.

Linda Vista Village is a 155-acre property comprised of five single family communities. It is located on both the north and south sides Linda Vista Boulevard just east of the Tucson Outlets and Twin Peaks Road. In addition to the single-family communities, other pads have been identified for multi-family and commercial uses. Concept plans currently have 265 single family lots with a variety of widths including 45’, 50’, 55’ and 60’. Lot depths will average 115’.

Market Overview

Lot Supply

The finished lot supply increased by 22 lots in Q1 to 3,118 due to an increased number of new lots introduced to the market. There were 580 new finished lots added in Q1: 128 lots in Blue Agave (Mattamy); 116 lots in Ridgeview (Mattamy); 78 lots in Tangerine Ridge (Pulte); 71 lots in Mountain Vail Ranch II (Richmond); 60 lots in Gladden Farms (Lennar); 58 lots in Gladden Farms (Richmond); 26 lots in La Estancia (Meritage); 13 lots in Andrada Ranch (Cornerstone); 12 lots in Haciendas at Wrightstown (Mesquite); and 10 lots in Estates at San Joaquin (Catland Properties LLC). During Q1 builders began construction on 558 new single family homes. This was 123 more home starts than last quarter and 12 more than Q2 2016, the highest quarterly number last year. This was also the most in a quarter since Q1 2010.

There are currently 18 single family communities (1,329 lots) in various stages of construction throughout Tucson. Of these up to 528 could be finished in Q2 2017. Up to eight new communities could be added next quarter and additional lots will be added to existing communities.

There are approximately 74 active SFR communities throughout the Tucson area. Six communities were built out in Q1, but are still selling the remaining specs: two in the NW, two in the Far South and one in each of the NE and SE submarkets

Lot Supply Statistics

| Q1 2017 | Q1 2016 | Q1 2015 | |

| Finished Lots | 3,118 | 3,146 | 3,643 |

| New Lots Added | 580 | 553 | 265 |

| Total New Lots Added prior 12 mo. |

1,980 |

1,161 |

1,136 |

| Total Quarter Permits | 794 | 620 | 470 |

SFR Community Statistics as of March 31, 2017:

▪ 77 active traditional SFR communities

▪ 6 communities were built-out or closed in Q1 (most still selling specs)

▪ 10 new communities were finished or opened in Q1 (some were additions to existing)

▪ 18 communities under construction (1,329 lots / up to 528 could be finished in Q2 ’17)

▪ up to 8 new communities could be added in Q2

▪ 15 residential land transactions in Q1 2017 totaling over $20.7 million

▪ 5 finished lot transactions

▪ 5 rolling options in 3 communities

▪ 1 investor land transactions – raw land for future development

▪ 4 platted lot transactions to builders – 2 in SE, 1 in SW and 1 in Far South

Lot Ownership

During Q1 2017 investor inventory increased by 10 lots while builder inventory increased by 9 lots.

▪ Builder controlled lots: 2,510 (80.5%)

▪ Investor controlled lots: 608 (19.5%)

Investor Ownership Q1 2017:

▪ 51.6% Far South submarket (206 lots)

▪ 15.6% Northwest submarket (257 lots)

▪ 13.5% Southeast submarket (106 lots)

▪ 13.5% Southwest submarket ( 39 lots)

Sales comp data from Real Estate Daily News – RED Comps (realestatedaily-news.com)

The Land Team of Dan Feig and Aaron Mendenhall at Chapman Lindsey Commercial Real Estate Services in Tucson can be contacted directly for additional insight and information at 520.747.4000

To read the full Q1 Tucson Land Update web version click here.