Q2 Tucson Land Report: Stronger Market, Fewer Lots

By Aaron Mendenhall, Chapman Lindsey Commercial Real Estate Services of Tucson

By Aaron Mendenhall, Chapman Lindsey Commercial Real Estate Services of Tucson

Improving Market Strains Lot Inventories

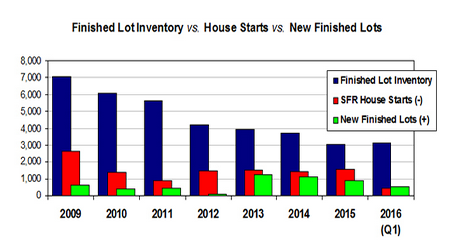

So far, 2016 has been a very encouraging year for home building in the Tucson area. Permits are up 25% over the first half of last year and new single family home starts are up 24%. The 966 new home starts in the first half of 2016 is greater than any first half since 2009 and Q2’s 546 starts is the most in a quarter since Q1 2010. We are on schedule to introduce over 1,700 new single family lots into the market this year, which will be the most since before the start of the recession.

While the number of new lots being delivered has been helping to maintain a relatively stable finished lot inventory number of around 3,100 lots for the past three quarters, this could change rapidly. As the permits and new home starts continue to strengthen, there will be increased pressure on the builders and developers to continue to deliver additional new lots.

Based on a 65% new single family home start to residential permit ratio and an increase of just 250 permits per year for the next 5 years, we can anticipate running out of finished lots in Tucson by 2020 if the market fails to average 1,400 new single family lots per year. To just keep up with the pace of new home starts, we will need to average 2,000 or more new lots per year.

Breaking down the numbers will demonstrate our current precarious position. Traditional single family new home starts have typically ranged between 60% and 75% of single family permits pulled in Pima County on an annual basis. The balance is in multi-family, active adult and custom homes started each year. For example, in 2015 there were 2,176 permits pulled and 1,545 new single family homes started or 71% of the permits pulled that year. In 2014 there were 2,284 permits pulled, but only 1,381 new single family house starts or 60.5% (December 2014 was when many builders pulled additional permits to take advantage of an impact fee moratorium in many subdivisions within the city of Tucson). Starts lag permits so these numbers do not correlate exactly, but over a multi-year analysis, it should be fairly representative.

Breaking down the numbers will demonstrate our current precarious position. Traditional single family new home starts have typically ranged between 60% and 75% of single family permits pulled in Pima County on an annual basis. The balance is in multi-family, active adult and custom homes started each year. For example, in 2015 there were 2,176 permits pulled and 1,545 new single family homes started or 71% of the permits pulled that year. In 2014 there were 2,284 permits pulled, but only 1,381 new single family house starts or 60.5% (December 2014 was when many builders pulled additional permits to take advantage of an impact fee moratorium in many subdivisions within the city of Tucson). Starts lag permits so these numbers do not correlate exactly, but over a multi-year analysis, it should be fairly representative.

This year we should easily see 2,500 permits pulled in the Tucson area. The number of new home starts should reach the 1,625 starts that would be needed to reach a 65% ratio. If we feel the market is recovering, it should not be a stretch to estimate a 250 permit increase in permits on an annual basis, particularly if we agree the target for a “normal” Tucson market would be 5,000 permits annually. With a 250 permit annual increase, we would reach 3,500 permits by 2020.

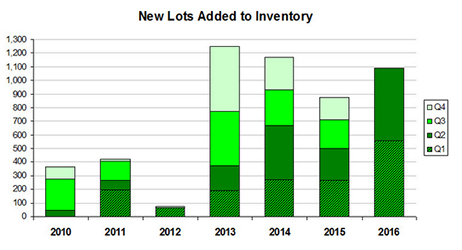

As mentioned, we should see around 1,700 new single family lots introduced into the market by the end of 2016. If this pace could be maintained or increased, the impending lot shortage could be minimized. However, looking at what is currently in the development pipeline, it will be difficult to achieve those same numbers in 2017. The first half of this year was strong with 1,091 new lots introduced. The second half should see about 620 new lots introduced, well off the pace of the first half. The lots currently under development that will not get finished in 2016 but should be introduced in 2017 total just over 800. There are another 600+ lots owned by builders that are either in the entitlement process or are being held for future phases of existing communities that should be introduced in 2018. Some of these lots could be accelerated and added to the 2017 lots, but it still appears to be unlikely that 2017 will be able to match the number of new lots introduced in 2016.

In 2015 builders purchased 19 properties with 1,281 platted lots plus raw or block platted land that could result in another 1,800 lots in the future (The majority of these future lots are in the Saguaro Bloom community purchased by DR Horton) . Of the 19 properties purchased, ten are already open for sales. Seven of these properties should open before the end of the year and only two have not yet begun development due to extended time frames of rezoning and entitlements. Of the 1,281 platted lots, 832 have already been fully developed. The remaining 449 lots should be developed and introduced to the market by the end of 2016.

So far in 2016 there have been 9 platted or raw land purchases by builders with a combined total of 621 platted lots. Five properties with 464 lots have already started to be developed. Of these, 132 could be developed in 2016. This would leave 485 to be introduced in 2017. Two of the transactions included raw land which will require rezoning and entitlements which will most likely push the estimated 450+ future lots into 2018.

We are only halfway into 2016, but unless a significant number of platted lot properties are purchased in the 2nd half, we will have a difficult time reaching 1,600+ new lots next year, much less matching the near 2,000 starts we could see if the market continues to improve at rates similar to what we have experienced the first half of 2016. Until we can start introducing at least as many, if not more new lots than what is being built on, inventories will plummet and the housing market could get extremely interesting pitting supply and demand against market tolerances or caps for pricing based on Tucson demographics. Exciting times lay ahead!

Market Overview

Lot Supply

The finished lot supply barely changed in Q2, only being reduced by 8 lots with a total finished lot count of 3,140. There were 538 new finished lots added to the market in Q2: 106 lots in CenterPointe at Vistoso (Maracay); 75 lots in Eagles Summit (Lennar); 120 lots in Estates at Capella (Meritage); 18 lots in Alamo Crossing (Mesquite); 52 lots in School Yard (Pepper-Viner); 51 lots in Sierra Morado (Pulte); 37 lots in Park Modern (Pepper-Viner); 46 lots in Villas Escalante (KB Home); and 33 lots in Camino Seco Village* (RB Price). Year to date, 1,091 new lots have been added to the market, which is 218 more than in all of 2015. This increase in new lots is much needed as builders continue to pull more permits and start more new homes. During Q2 builders began construction on 546 new single family homes, 126 more than in Q1 and the most starts since Q1 2010.

There are currently 14 communities (1,354 SFR lots) under construction throughout Tucson. Of these up to 508 lots could be completed in Q3 2016. Four new communities could be added next quarter and additional lots will be added to existing communities.

There are approximately 74 active SFR communities in the Tucson Metro area. Nine communities were built out during the quarter, but still selling the remaining specs: 4 in the NW, 2 in the SE, 2 in the SW and 1 in the Far South submarket. As many as 12 more communities could build out in Q3 2016 based on recent building trends.

*Communities not yet open for sales

Lot Supply Statistics

Q2 ’16 vs. Q2 ’15 vs. Q2 ’14

Finished Lots: 3,140 / 3,420 / 3,811

New Lots Added: 538 / 236 / 365

Total New Lots Added – prior 12 mo: 1,463 / 1,007 / 1,510

Total Quarter Permits * 750 / 622 / 617

SFR Community Statistics as of March 31, 2016:

- 76 active traditional SFR communities

- 9 communities were built-out or closed in Q2 (most still selling specs)

- 7 new communities were finished or opened in Q2

- 2 communities added additional lots to existing inventory

- 14 communities under construction (1,354 lots / up to 508 could be finished in Q3)

- up to 4 new communities could be added in Q3

- other future lots will be additions to existing communities

- 12 residential land transactions in Q2 2016 totaling over $14 million

- no finished lot transactions

- 5 rolling options in 2 communities

- 2 investor land transactions – 1 platted, 1 raw land for future development

- 5 platted lot transactions to builders – 4 in NW and 1 in SE Tucson

Lot Ownership

During Q2 2016 investor inventory increased by 33 lots in Camino Seco Village.

- Builder controlled lots: 2,230 (71.0%)

- Investor controlled lots: 910 (29.0%)

Investor Ownership Q2 2016:

- 0% Far South submarket (255 lots)

- 9% Northwest submarket (405 lots)

- 9% Southeast submarket (210 lots)

- 4% Southwest submarket ( 40 lots)

Forecast

Permits continued to outpace expectations through Q2 with 750 permits pulled in the quarter. June’s 275 total was the highest monthly total of the year and only January has had less than 200 permits pulled so far this year. The 1,370 permits pulled in the first half of the year is well ahead of the 1,092 in the first half of 2015. It also outpaces the 1,135 of 2014 and 1,209 of 2013. Should the trend of 200+ permits per month continue, we should easily pass 2,500 permits this year.

Homebuilders are continuing to start an increased number of single family new homes throughout the Tucson area. New home starts in Q2 increased over Q1 by 126 starts for a total of 546 new home starts in the quarter and 966 for the first half of the year.

We anticipate Q3 to be slightly lower in permits than the stellar Q2 we just experienced. However, based on recent permit activity and the new communities coming online, we anticipate 2016 finishing above expectations.

Our lot supply numbers represent only traditional SFR lots. We do not track multi-family, active-adult, or custom lots. Our definition of a ‘finished’ lot is one that is fully improved and a building permit can be pulled. Lots are no longer considered available once trenching has been initiated. Sales do not affect our counts – only starts. Builder lots include all lots under their control, including options.

We currently do not include platted lots in our inventory or ownership counts. However, there is an increasing amount of activity from both builders and investors in acquiring raw and entitled land in the Tucson area. We do track them and will include them in our counts as they are developed.

Investor lots include investors, developers and other non-builders.

(*) Permit data from Bright Future Real Estate Research, LLC; Sales comp data from Real Estate Daily News Comps (realestatedaily-news.com); Home builder sales data from SAHBA (sahba.org)

About Our Company

CHAPMAN LINDSEY Commercial Real Estate Services, L.L.C. was formed in 1991 by successful real estate professionals who wanted to better serve their clients. As a full service commercial real estate company, CHAPMAN LINDSEY offers brokerage and leasing services with an emphasis in vacant land sales. CHAPMAN LINDSEY’s three partners combine over 76 years of commercial real estate experience to provide a focus of expertise in the areas of land, investment properties, property

leasing, acquisition and deposition services, and tenant representation.

The company is an active member of the Southern Arizona CCIM (Certified Commercial Investment Member) Chapter and the Tucson Association of Realtors.

Dan Feig and Aaron Mendenhall specialize in the sale of land and developed lots to investors, developers and home builders in Pima County.

Highlights

- CHAPMAN LINDSEY has closed over $600 million in transactions.

- CHAPMAN LINDSEY has also closed over $125 million in land alone in the past 6 years.

- CHAPMAN LINDSEY has exclusively represented the following home builders with the purchase or sale of their own land/excess inventory;

Cornerstone Homes, DR Horton Homes, Ducati Homes, KB Home, Lennar Homes, LGI Homes, Maracay Homes, Meritage Homes, Milestone Homes, Miramonte Homes, Pepper-Viner Homes, Richmond American Homes, Standard Pacific Homes and TJ Bednar Homes

For additional information Daniel Feig should be reached at 520-747-4000 x103 and Aaron Mendenhall at 520-747-4000 x102

For full report with more graphs: CLICK HERE