TUCSON, AZ (June 25, 2026) — Tucson’s job market softened in May, giving back much of April’s payroll gain and underscoring the region’s uneven employment recovery compared with the state and Phoenix metro area.

The Tucson metro area posted 407,400 nonfarm payroll jobs in May 2026, down from a revised 409,300 jobs in April, a decline of approximately 1,900 jobs for the month, according to the latest employment data from the U.S. Bureau of Labor Statistics. Year over year, Tucson employment was essentially flat, with BLS reporting a 0.0% change from May 2025.

The largest monthly decline came from government employment, which fell from 80,100 jobs in April to 78,500 jobs in May, a drop of about 1,600 jobs. Professional and business services also declined, falling from 49,700 jobs in April to 49,000 in May.

The May report reverses the short-term improvement Tucson posted in April, when the region added jobs after a slower start to the year. While one month does not define a trend, the May numbers show that Tucson has not yet turned monthly payroll gains into sustained year-over-year job growth.

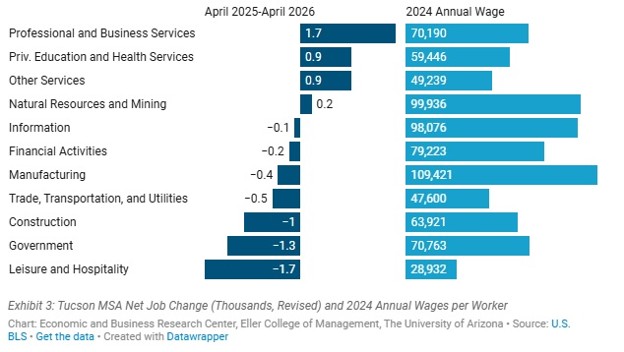

Tucson MSA Net Job Change, in Thousands, and 2024 Annual Wages per Worker

Note: Chart reflects April 2025–April 2026 revised net job change, not the May monthly payroll release.

The Tucson chart helps explain why the May decline matters by showing which sectors were already gaining or losing jobs heading into the May payroll report. Tucson’s employment base remains heavily weighted toward government, education, health care, and service-related sectors, while higher-wage private-sector job growth remains more difficult to sustain.

Several sectors did show improvement in May. Construction rose from 20,000 jobs in April to 20,400 in May, while manufacturing increased from 28,600 to 28,900. Mining and logging also edged higher, rising to 3,000 jobs. Education and health services, one of Tucson’s largest private-sector employment categories, held steady at 75,600 jobs.

That mix matters. Gains in construction, manufacturing and mining are more closely tied to private-sector investment and production than government hiring, making the May increases notable even as total payroll employment declined.

Year over year, Tucson’s strongest percentage gains were in mining and logging, other services, professional and business services, education and health services, and information. However, those gains were offset by continued weakness in leisure and hospitality, financial activities, trade, transportation and utilities, construction, manufacturing, and government.

The labor-force picture should be read separately from the payroll survey because it comes from the household survey and may vary by source table, revision status, and seasonal adjustment. The Arizona Office of Economic Opportunity table included below shows changes in Tucson’s civilian labor force, employment, unemployment, and unemployment rate, while the BLS’s Tucson “At a Glance” page reports a different preliminary May labor-force series. The broader takeaway is that the household-survey data should be used as context, not mixed directly with the payroll-job totals.

Phoenix also posted a month-over-month payroll decline in May, but continued to show stronger year-over-year momentum. The Phoenix-Mesa-Chandler metro area recorded 2,480,800 nonfarm payroll jobs in May, down from 2,491,400 in April, but up 1.0% from a year earlier. Tucson, by contrast, remained flat year over year.

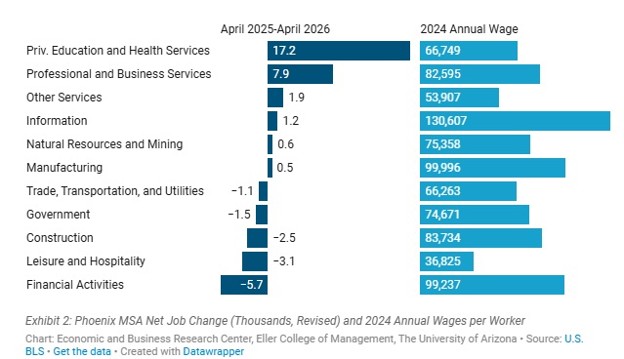

Phoenix MSA Net Job Change, in Thousands (revised) and 2024 Annual Wages per Worker

Note: Chart reflects April 2025–April 2026 revised net job change, not the May monthly payroll release.

The Phoenix chart provides important context for Southern Arizona. Even when Phoenix experiences monthly volatility, the state’s largest metro area continues to post stronger year-over-year job growth than Tucson. That gap matters because employment growth drives household formation, consumer spending, demand for commercial space and long-term regional competitiveness.

Statewide, Arizona’s seasonally adjusted unemployment rate increased to 4.8% in May from 4.7% in April, while the U.S. unemployment rate remained at 4.3%. Arizona’s seasonally adjusted labor force declined by 15,470 individuals over the month and was down 49,805 individuals from a year earlier, according to the Arizona Office of Economic Opportunity.

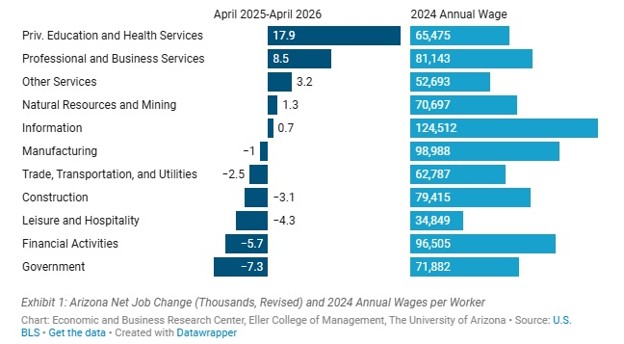

Arizona Net Job Change, in Thousands, Revised, and 2024 Annual Wages per Worker

Note: Chart reflects April 2025–April 2026 revised net job change, not the May monthly payroll release.

The statewide chart reinforces the broader trend: Arizona’s job market has cooled, and job gains have become more uneven across industries and regions. Tucson’s challenge is not simply the May decline, but the need to compete more effectively for higher-wage private-sector employment in a slower statewide labor market.

For Southern Arizona, the May jobs report reinforces a familiar economic development challenge. Tucson has significant assets, including the University of Arizona, aerospace and defense, cross-border trade, bioscience, optics, and a growing technology and innovation ecosystem. But the region’s job growth continues to lag the pace needed to close the gap with faster-growing markets.

The numbers also highlight the importance of private-sector job creation. Government, education, health care, and defense-related employment provide Tucson with stability, but the region’s long-term competitiveness will depend on its ability to attract and grow employers in higher-wage, scalable industries.

For Tucson to compete more effectively for higher-wage private-sector employment, regional leadership will need to move in the same direction on infrastructure, land readiness, permitting, workforce development, and business attraction.

Bottom line: Tucson’s May jobs report was not bad, but it was uneven. The region gave back some of April’s payroll gain and remained flat year over year, but May also brought increases in construction, manufacturing, and mining sectors more closely tied to private investment and production. The report reinforces the urgency of business attraction, infrastructure readiness, workforce development, and stronger alignment among public, private, and regional leadership.

The following table provides a household-survey labor force comparison between Tucson and Phoenix from the Arizona Office of Economic Opportunity. It should be read separately from the payroll employment figures discussed above.

Notes:

Figures are reported in thousands. Labor force, unemployment, total employment, and unadjusted unemployment rates are produced by the Local Area Unemployment Statistics program in the Arizona Office of Employment and Population Statistics, in cooperation with the U.S. Department of Labor, Bureau of Labor Statistics. BLS data used as part of the input in producing LAUS data come from the monthly Household Survey, produced by the Census Bureau for the U.S. Department of Labor, Bureau of Labor Statistics. Preliminary, revised, seasonally adjusted, and not seasonally adjusted data are identified in the source tables. MSA refers to Metropolitan Statistical Area.

(c) Preliminary; (d) Revised.