TUCSON, AZ (April 28, 2026) — Tucson’s multifamily market entered 2026 with improving vacancy, cautious underwriting, and continued investor interest in older value-add assets, according to Cushman & Wakefield | PICOR’s Q1 2026 Multifamily Marketbeat report.

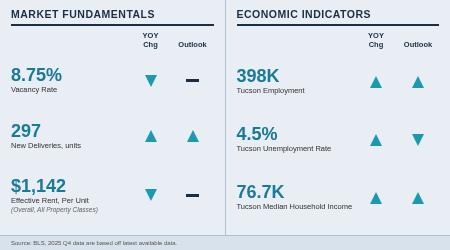

Market vacancy declined to 8.75% in the first quarter, with improvement reported across 10 of Tucson’s 15 submarkets. Oro Valley/Catalina posted one of the strongest vacancy readings at 6.12%, while Southeast Tucson remained the softest submarket with a vacancy rate of 14.24%.

Average effective rent for the Tucson market was $1,142 per unit, down slightly year-over-year but up from the previous quarter, suggesting rents may be stabilizing after a softer period. The University submarket recorded the highest rent growth, up 19.28% year-over-year, with average effective rent of $1,442 per unit.

Investment activity remained selective. The report noted just seven arm’s-length transactions of 40 units or more during the quarter, as buyers continued to underwrite more conservatively. Mid-sized properties continued to trade, particularly older assets with value-add potential. Properties offering seller financing drew stronger demand and achieved higher pricing, reflecting the continued challenge of conventional financing.

Financing remained a key factor in the market. Interest rates briefly dipped below 6% in late February before rising again amid global market volatility. Tucson multifamily originations averaged a 6.04% interest rate and 71.06% combined loan-to-value during the quarter, excluding 1031 exchange down payments. Insurance costs also remained a headwind, especially for older properties and buildings with multiple units.

On the leasing side, owners and managers focused on maintaining occupancy and attracting qualified tenants. The report noted longer lease-up times for renovated units, more budget-conscious renters, and the growing use of move-in promotions and discounted deposits to encourage leasing decisions.

Tucson’s broader economy remained generally steady entering 2026. Median household income rose year-over-year to $76,700, employment held near 398,000 jobs, and unemployment was reported at 4.5%. Cushman & Wakefield | PICOR noted that Tucson’s income gains, resilient job base, and continued household and population growth continue to support modest momentum in the multifamily sector.

Looking ahead, the report described the market as cautiously positive, with demand strongest for well-located properties near recent commercial and retail growth. Assets in less desirable locations may require higher cap rates or creative financing to attract buyers. Long-term demand is expected to remain supported by Tucson’s I-10 corridor, the University of Arizona, and major economic development activity, including the planned Project Blue data center.

See the full report here.