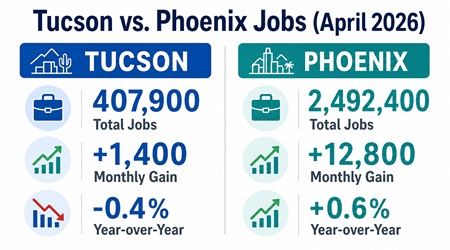

TUCSON, AZ (May 29, 2026) — Tucson added jobs in April, but the region continued to trail Phoenix and the state in year-over-year employment growth, according to the latest employment data released May 21, 2026, from the Arizona Office of Economic Opportunity and U.S. Bureau of Labor Statistics.

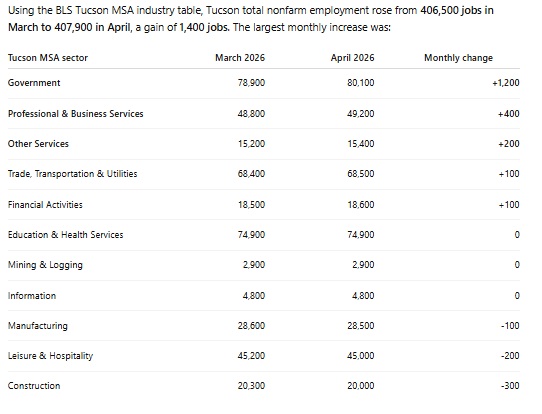

The Tucson metro area posted 407,900 nonfarm jobs in April 2026, up from 406,500 jobs in March, a gain of approximately 1,400 jobs for the month, with about 1,200 in government. Tucson remained slightly below its year-earlier level, with total nonfarm employment down 0.4% from April 2025. That equates to an estimated loss of roughly 1,600 jobs year over year.

Phoenix, by comparison, recorded 2,492,400 nonfarm jobs in April 2026, up from 2,479,600 in March, a gain of approximately 12,800 jobs for the month. Unlike Tucson, the Phoenix metro area was also up year over year, with employment increasing 0.6% from April 2025.

The contrast highlights the different scale and momentum of Arizona’s two largest metro economies. Tucson’s April increase shows some short-term improvement, but the region has not yet matched Phoenix’s ability to generate sustained year-over-year job growth.

Statewide, Arizona added 16,300 not-seasonally adjusted nonfarm jobs from March to April, according to the Arizona Office of Economic Opportunity’s April employment report. The state’s seasonally adjusted unemployment rate held at 4.7%, while the U.S. unemployment rate was 4.3%.

For Tucson, the data present a mixed picture. The month-over-month gain is positive, especially after a period of slower employment growth, but the year-over-year decline suggests the region is still experiencing softer job creation than in Phoenix and the state overall.

Phoenix’s larger employment base gives it a natural advantage in raw job gains, but its positive year-over-year growth also reflects continued expansion in sectors tied to population growth, corporate investment, logistics, health care, advanced manufacturing, and technology-related development.

Tucson’s economy remains more concentrated in government, education, health care, defense, and university-related activity. Those sectors provide stability, but they do not always produce the same level of rapid private-sector job growth seen in the Phoenix metro.

The April report underscores a central economic development challenge for Southern Arizona: Tucson is adding jobs, but not yet at the pace needed to close the gap with Phoenix or capture a larger share of Arizona’s growth.

For regional leaders, the numbers reinforce the importance of business attraction, infrastructure readiness, workforce development, and site availability. Tucson’s competitive advantages remain significant, including its university research base, defense and aerospace presence, cross-border trade position, and relative affordability. But the latest jobs data shows that converting those advantages into faster employment growth remains an unfinished task.

Bottom line: Tucson gained jobs in April, but Phoenix continues to carry more of Arizona’s employment momentum. Tucson’s challenge is not simply to grow, but to grow consistently enough to turn monthly gains into sustained year-over-year expansion.