CBRE: Phoenix Office Market Gains Momentum as Vacancy Tightens in Q2 2026

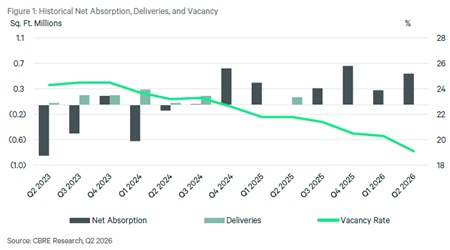

PHOENIX, AZ (July 14, 2026) — The Greater Phoenix office market continued to strengthen during the second quarter of 2026, posting nearly 490,000 square feet of positive net absorption as vacancy declined and asking rents moved higher.

PHOENIX, AZ (July 14, 2026) — The Greater Phoenix office market continued to strengthen during the second quarter of 2026, posting nearly 490,000 square feet of positive net absorption as vacancy declined and asking rents moved higher.

Phoenix ended the quarter with an overall office vacancy rate of 19.1%, down 120 basis points from the first quarter and 270 basis points from a year earlier. Availability also tightened to 22.8%, while the average direct asking rate increased to $32.30 per square foot, full-service gross.

The improvement represents a substantial shift from the contraction experienced three years ago, when quarterly net absorption stood at negative 798,000 square feet. Second-quarter absorption improved by approximately 263,000 square feet from the previous quarter and by 488,000 square feet year over year.

Class B properties accounted for most of the quarter’s gains, recording 398,000 square feet of net absorption. Class A properties added 79,000 square feet, while Class C buildings posted 13,000 square feet of positive absorption. Year-to-date absorption across the market reached 717,000 square feet.

The positive activity was concentrated largely in the suburban market, which posted 467,000 square feet of quarterly absorption and an overall vacancy rate of 17.6%. By comparison, the urban market recorded 23,000 square feet of absorption and remained considerably softer, with vacancy of 27.3%.

Northeast Valley/Scottsdale led the region with 272,000 square feet of net absorption and the lowest vacancy rate among the major submarkets at 14.1%. West/Northwest Phoenix followed with 176,000 square feet of absorption and vacancy of 15.2%.

The Southeast Valley added 70,000 square feet, while the Central Business District recorded a modest 23,000-square-foot gain. Camelback/Piestewa Peak and Tempe were the only major submarkets to finish the quarter with negative absorption, posting losses of 42,000 square feet and 28,000 square feet, respectively.

Demand also continued to favor higher-quality office space. Class A vacancy declined to 19.3%, while Class B vacancy finished at 19.4%. Both were substantially lower than three years earlier. Class C vacancy stood at 17.1%, but was higher than its level in the second quarter of 2023, reflecting the market’s ongoing preference for better-located and higher-amenity properties.

Average asking rents increased 0.7% during the quarter and 3.4% from a year earlier. Class A space commanded an average of $41.66 per square foot, compared with $30.60 for Class B and $22.05 for Class C.

By submarket, Tempe posted the highest overall asking rate at $40.17 per square foot, followed by Camelback/Piestewa Peak at $39.27 and Northeast Valley/Scottsdale at $36.46. The Central Business District remained the most affordable major submarket, with an average asking rate of $28.87 per square foot.

Leasing activity totaled approximately 1.1 million square feet, representing a 14.6% increase from the first quarter, although activity remained 4.9% below the same period last year. Northeast Valley/Scottsdale was the most active submarket with 354,000 square feet of leasing, followed by the Southeast Valley with 175,000 square feet.

The quarter’s largest transaction was Consumer Cellular’s new 123,000-square-foot lease at 8501 E. Raintree Drive in Scottsdale. Valley Metro Rail renewed 70,000 square feet at 101 N. First Avenue in downtown Phoenix, and an undisclosed tenant leased 61,000 square feet in the Northeast Valley/Scottsdale submarket.

Other notable transactions included AssistRx’s 49,790-square-foot lease in the Southeast Valley, Southwest Service Administrators’ 47,000-square-foot renewal in West/Northwest Phoenix, Northrop Grumman’s 46,000-square-foot renewal and Honeywell’s 29,000-square-foot lease in East Phoenix.

New construction remained limited, with 450,525 square feet underway and no office deliveries during the quarter. Nearly all construction was concentrated in Northeast Valley/Scottsdale, where the Republic Services and Sprouts corporate headquarters projects accounted for approximately 410,525 square feet.

The remaining 40,000 square feet was under construction at The Grove-4210 in the Camelback/Piestewa Peak submarket. The fully preleased project is expected to deliver during the third quarter.

With positive absorption, falling vacancy and restrained construction, the Phoenix office market entered the second half of 2026 with improving fundamentals. However, conditions remain uneven, with suburban locations and higher-quality buildings continuing to outperform downtown and older office properties.