CBRE Report: Phoenix Moves Ahead of Silicon Valley in Data Center Inventory

Phoenix saw a 238% increase year over year in data center absorption

Phoenix saw a 238% increase year over year in data center absorption

PHOENIX – (August 28, 2024) – Phoenix’s data center supply grew by 150.8 megawatts (MW) in the first half of the year as developers delivered more capacity to meet growing demand, according to CBRE’s latest North American Data Center Trend Report.

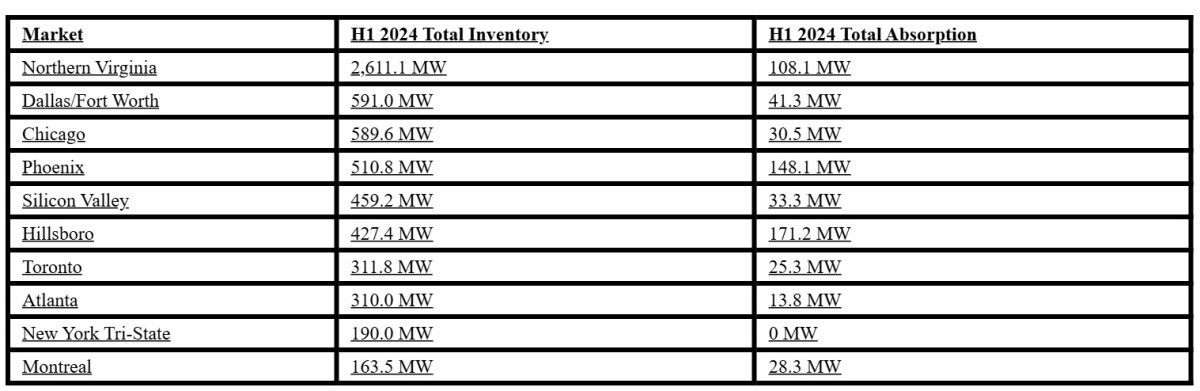

Phoenix’s total inventory increased to 510.0 MW (a 44% increase year over year), leaping ahead of Silicon Valley for the first time to rank fourth largest among primary North American data center markets. The market shows no signs of slowing down, with 334.3 MW of product currently under construction in the Valley—the most since 2016.

Phoenix’s vacancy rate edged slightly down from last year’s second half to 3.3%, much in part to the 148.1 MW of positive absorption in H1 2024, a 238% increase year over year. Rental rates remained firm due to reductions in available supply and power. Lease renewal rental rates increased by as much as 20%.

“The Phoenix data center market is continuing to experience unprecedented growth, driven by significant investments from major tech companies,” said Mark Krison, executive vice president at CBRE in Phoenix. “The demand for data center space continues to surge, fueled by the increasing need for cloud services and AI capabilities. This growth is highlighted in Phoenix’s increase in supply and its emergence as a leading hub in the industry compared to other West Coast markets.”

Across North America, 515.0 MW of new supply were added in the eight primary North American data center markets in H1 2024, equivalent to adding the entirety of Silicon Valley’s existing inventory. That first-half construction increased the eight-market inventory of data center space by 10% from year-end 2023 and 24% (1,100.5 MW) a year ago.

National average rental rates rose to $174.06 per kW/month (a 6.5% increase from H2 2023) due to limited supply and strong demand. Atlanta saw the most significant pricing increase across primary markets, growing 26% year over year due to demand from AI usage. Phoenix led primary data center markets in average asking rates at $170 – $210 per kW/month. Prices nationally are expected to increase in the second half of 2024 as rising construction and equipment costs continue to affect the sector.

The demand for high-powered computing has exacerbated the pricing disparity between legacy facilities and new data centers, partially because older data centers don’t have the infrastructure to handle the power demands of today’s users. This trend is likely to persist, opening the door for tertiary markets like Northern Indiana, Idaho, Arkansas, and Kansas to draw interest from hyperscalers and developers due to available land and power availability.

Top 10 Largest Markets

To view the full report, click here.

*The eight primary U.S. data center markets are Northern Virginia, Dallas/Fort Worth, Silicon Valley, Chicago, Phoenix, New York Tri-State, Atlanta and Hillsboro.