CBRE Tucson: Industrial Vacancy Tightens as Leasing Activity Starts the Year Off Strong

![]() TUCSON, ARIZONA, April 14, 2023 – CBRE’s Research Team is reporting Tucson Industrial vacancy decreased 120 basis points (bps) quarter-over-quarter to 2.5% in Q1 2023. The industrial market captured 389,500 square feet of gross absorption, bolstered by activity in the Southeast submarket.

TUCSON, ARIZONA, April 14, 2023 – CBRE’s Research Team is reporting Tucson Industrial vacancy decreased 120 basis points (bps) quarter-over-quarter to 2.5% in Q1 2023. The industrial market captured 389,500 square feet of gross absorption, bolstered by activity in the Southeast submarket.

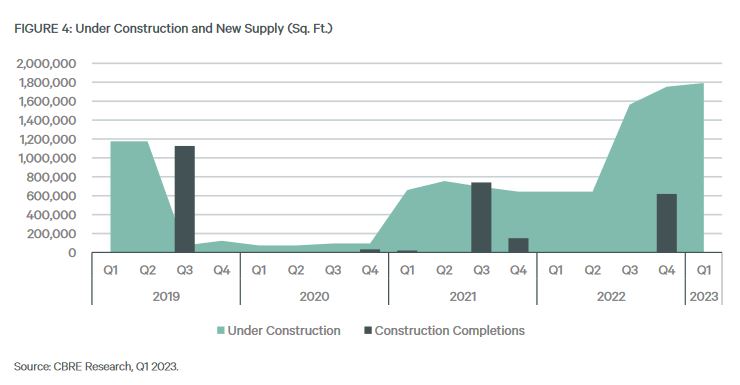

- Total construction activity increased slightly to 40,000 square feet, with no deliveries in Q1 2023.

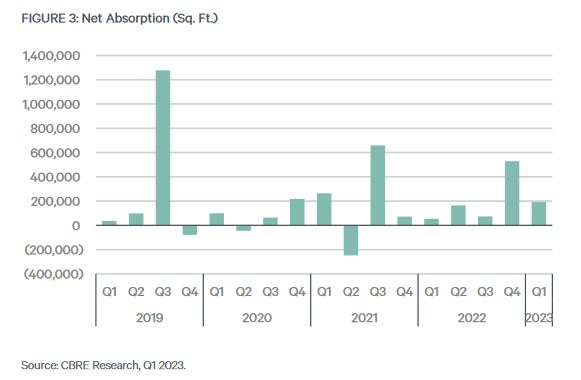

- The Tucson industrial market had healthy leasing activity with 389,500 square feet of gross While renewals dominated market activity, new leases pushed net absorption to 191,465 square feet in Q1 2023.

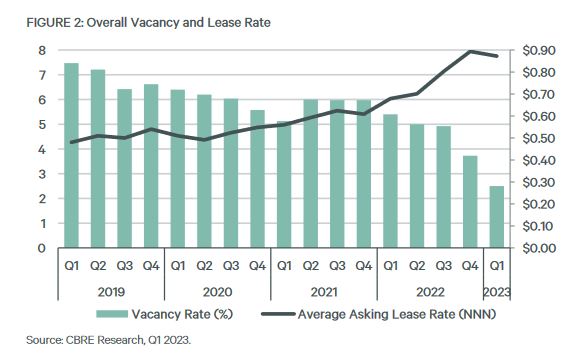

- The vacancy rate dropped to 2.5% as new leases outpaced move-outs in Q1 2023. The decrease in vacancies was also a result of the lack of new product deliveries in the first quarter.

- Under-construction projects located in the Northwest and Airport submarket are anticipated to deliver in Q2 2023. Lastly, the direct average asking NNN lease rates remained nearly flat at $0.87 per square foot.

Availability and Vacancy

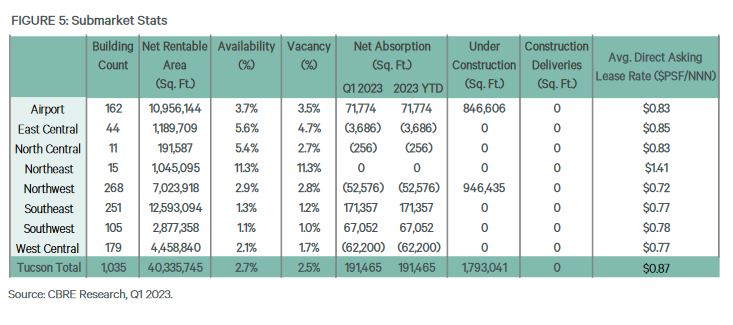

Tucson’s Industrial space availability decreased to 2.7%, equivalent to 1.1 million sq. ft. of space at the end of Q1 2023. Availability in the Airport submarket declined to 3.7% with multiple large new leases. The Northwestern submarket’s availability rate of 2.9% was slightly higher than the Tucson average, but the submarket remains a sought-after submarket due to interstate access and proximity to Phoenix. Space available in the Southeast submarket remained scarce, with 1.3% available.

Tucson’s total vacancy declined to 2.5% in Q1 2023 with 1.0 million sq. ft. of vacant space. The vacancy rate in the Airport submarket had a quarter-over-quarter decrease of 20 basis points to 3.5% while the Northwest submarket vacancy increased 80 bps to 2.8%. The Southeast submarket vacancy remained tight at 1.2% and remained a desirable market for distribution and manufacturing operations.

Lease Rates

The direct average asking NNN lease rate increased $0.19 year-over-year to $0.87 per sq. ft. in Q1 2023—a 28.4% increase year-over-year. Asking rates within the Southeast submarket increased to $0.78, which represented the most notable rate change. Decreased availability in this submarket continued to put upward pressure on asking rates. The Airport submarket recorded a minor increase in NNN asking lease rate at $0.83 per sq. ft. With an average asking lease rate of $0.72 per sq. ft., the Northwest submarket offers tenants a cost-efficient and geographically advantageous option.

Net Absorption and Leasing Activity

The Tucson industrial market had 191,465 sq. ft. of positive net absorption in Q1 2023, driven primarily by the Southeast and Airport submarkets. The Southeast submarket recorded 171,357 sq. ft. of net absorption. The Airport submarket recorded 101,774 sq. ft. of leasing activity, with a 65,303 sq. ft. lease signed by Cactus Portable Storage and an owner-user building acquisition at 2425 E Medina Rd. The Southwest submarket recorded a notable 65,250 sq. ft. warehouse leased by Pima County.

The West Central submarket offset the positive net absorption in the market due to the 60,000-square-foot move out of Sam Levitz Furniture Company. The Northwestern submarket followed closely behind with 52,576 square feet of negative net absorption.

Development Activity

No projects were delivered in Q1 2023, but construction continued for the 1.8 million sq. ft. of industrial product. The 946,415 square feet from buildings 1 and 2 of the Southern Arizona Logistics Center made significant development progress in the Northwestern submarket and are expected to deliver in Q2 2023. The 40,000-square-foot Campbell Landing project is near completion as well. The four-building project will serve a much-desired space requirement for tenants looking to fill up to 10,000 square feet. The 806,000-square-foot Tucson Commerce Center in the Airport submarket is expected to deliver in late 2023. Many projects, such as the remaining Southern Arizona Logistics Center buildings, I-10 International, and the newly announced Southern Arizona Regional, remain planned and await construction start dates.

Outlook

The Tucson industrial market has had several quarters of consistent growth and these trends are expected to continue in subsequent quarters. With sustained record low vacancy and a

strong construction pipeline, Tucson is expected to capitalize on tenants looking to establish or expand operations in the Sun Belt. Prospective projects like American Battery Factory’s new

manufacturing facility, going in at the Pima County Aerospace Campus near Raytheon, will continue to place the spotlight on Tucson as an optimal manufacturing location further sustaining demand.

Read full Industrial Report Q1 2023 here.