Phoenix Office Market Extends Recovery in First Quarter as Vacancy Falls and Demand Remains Positive

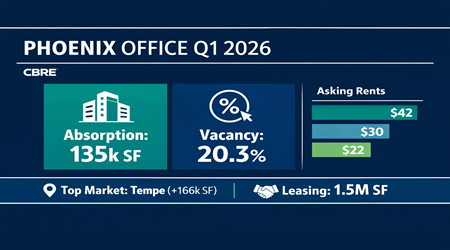

PHOENIX, AZ (April 14, 2026) — The Phoenix office market continued its recovery in the first quarter of 2026, posting 135,807 square feet of positive net absorption as vacancy declined to 20.3 percent, according to CBRE’s first-quarter office figures report. The latest quarter adds to a broader turnaround that has followed the market’s sharp correction in 2023, with annual net absorption improving from roughly negative 1.4 million square feet in 2023 to more than 1.3 million square feet of positive absorption in 2025.

CBRE reported that the Phoenix vacancy rate has now dropped from 23.9 percent in the first quarter of 2024 to 20.3 percent in the first quarter of 2026, while availability has also tightened to 23.3 percent. Although quarterly absorption slowed from the unusually strong 749,729 square feet recorded in the fourth quarter of 2025, the market remained in positive territory, signaling that tenant demand continues to support a gradual rebound. Average direct asking lease rates rose to $32.09 per square foot full service, up 2.4 percent from the prior quarter and 2.5 percent year-over-year.

The quarter showed a split between product classes. Class B office properties carried much of the market’s leasing momentum, posting 314,836 square feet of positive net absorption, while Class A and Class C space combined for 179,029 square feet of negative absorption during the quarter. Even so, Class A space has remained a major part of the longer-term recovery, with nearly 891,288 square feet of net absorption over the last four quarters. Asking rents for Class A space climbed to $42.02 per square foot, compared with $30.29 for Class B and $22.60 for Class C.

Performance varied widely by submarket. Tempe led the metro in first-quarter net absorption with 166,031 square feet, followed by the Southeast Valley with 144,585 square feet and East Phoenix with 85,660 square feet. On the other side of the ledger, the CBD posted negative 144,884 square feet of absorption, while Northeast Valley/Scottsdale recorded negative 136,978 square feet, and Camelback/Piestewa Peak slipped by 13,009 square feet. Tempe also commanded the metro’s highest asking rents at $39.74 per square foot, closely followed by Camelback/Piestewa Peak at $39.63 per square foot.

Leasing volume remained active even as it moderated from the prior quarter. Gross leasing activity totaled 1.5 million square feet in the first quarter, with 6.2 million square feet leased over the last four quarters. Southeast Valley and Northeast Valley/Scottsdale posted the highest leasing totals, while notable transactions included Maricopa County Community College taking 94,480 square feet at two Southeast Valley locations, IES Communications leasing 56,680 square feet in East Phoenix, Concorde Career Colleges taking 52,702 square feet in West/Northwest Phoenix, and Waymo leasing 40,357 square feet in Tempe.

Construction remained restrained, which has helped support the market’s improving fundamentals. CBRE reported 450,525 square feet under construction at the end of the first quarter, with no new office deliveries recorded during the period. The largest projects underway include The Grove – 4210, along with the Sprouts and Republic Services corporate headquarters at CityNorth. CBRE noted that tightening Class A conditions and continued demand for top-tier product may increase the need for premier multi-tenant space and future luxury build-to-suit opportunities for companies considering Phoenix as their headquarters.

Overall, the first-quarter numbers suggest Phoenix’s office market is moving further away from its post-pandemic correction and into a more stable phase marked by measured construction, rising rents, and steady tenant demand. While some major submarkets continue to face elevated vacancy and uneven performance, the broader direction points to a market that is gradually regaining balance.

Read the full report here: CBRE Phoenix Office Report Q1 2026