As homes become even more unaffordable with rising mortgage rates and resulting crushed application volumes, you might think that demand for apartments would be screamingly hot. And it is—or was until the third quarter. The story coming out a Newmark report is surprising, because it suggests a possible sea change in how multifamily has been performing.

As homes become even more unaffordable with rising mortgage rates and resulting crushed application volumes, you might think that demand for apartments would be screamingly hot. And it is—or was until the third quarter. The story coming out a Newmark report is surprising, because it suggests a possible sea change in how multifamily has been performing.

- Following extraordinary property level fundamentals in 2021, quarterly absorption posted net negative demand of 82,035 units nationally in the third quarter of 2022, during the historically active leasing months of July, August and September, where absorption was negative.

- Housing remains undersupplied, with a 400,000-unit shortfall in 2021, when comparing single-family and multifamily completions to new households established. The lack of supply has resulted in an annual average effective rent growth of 13.5% as of the third quarter of 2022, 1,070 basis points above the long-term average.

- Nationally, vacancies remain near historic lows of 3.1% on a trailing 12-month basis; however, quarter-over-quarter vacancies have risen 90 basis points as demand has trailed off recently. The Class A and Class B segments have suffered the most as of late, with 194 and 200 basis point declines, respectively, in year-over-year occupancy as of September.

- The 30-year fixed-rate mortgage average rose to 6.7% in the third quarter of 2022, increasing 122.6% year-over-year, further adding to the elevated cost of single-family homes. As interest rates have climbed, mortgage applications have fallen 65.3% year-over-year as of September.

- Multifamily loan origination volume year-to-date totaled $228.8 billion, with a significant drop off in activity since May 2022. Continued volatility in the debt markets, the highest inflation in 40 years, sharp interest rate increases and war in Ukraine have materially impacted both investment sales and financing markets in the third quarter of 2022.

- While multifamily remains the most sought-out property type, accounting for 41.7% of all US commercial real estate year-to-date, sales volume in the third quarter of 2022 declined 17.2% year-over-year, to $74.1 billion. Compared with the first three quarters of 2021, sales volume has increased 25.0% and deal size continues to escalate.

- Nominal cap rates increased 55 basis points quarter-over-quarter according to Green Street Advisors; however, transactional cap rates have continued to compress in the third quarter of 2022, ticking down 4 basis points to 3.93% nationally. The sub-4% yield remains problematic as debt costs have risen substantially, and valuations between buyers and sellers remain far apart.

What We Expect

- After two consecutive quarters of negative net absorption, the fourth quarter of 2022 is likely to see positive absorption. Vacancy is expected to increase in the coming quarters, as demand remains muted and deliveries increase. Recently adjusted rental growth projections for 2023 to 4.4% from 9.5%, partially based on lower levels of demand, may be offset by persistent inflation.

- Single-family home purchases will remain prohibitive, as substantially higher costs of borrowing is likely to increase near term as the Federal Reserve tries to combat inflation. Additionally, a potential contraction in the economy, paired with recently announced layoffs, will further sideline would-be buyers, even as prices retreat. While a worsening economy will impact the rental market, as well, fewer homebuyers means more renters.

- Market dislocation, combined with further rate hikes, will materially impact investment sales and origination volumes in the fourth quarter of 2022 and into 2023. Nonetheless, the fourth quarter of 2022 should see a host of transactions close that have been under contract for an extended period, particularly those with pricing adjustments.

- Lagging markets such as New York and San Francisco that have underperformed, given the severity of the pandemic and subsequent COVID-19-related restrictions, should experience above-average fundamentals as a rotation is underway, with fast-growing markets, particularly throughout the Sun Belt, set to normalize.

- While the largest nontraded REITs remain well-capitalized presently, a sharp decline in fundraising and uptick in redemptions may result in reduction in activity in the core and core-plus market segments, where they’ve been the largest buyers over the past few years.

- Conversions from older vintage commercial properties to multifamily will grow in the years ahead; however, it will not be immediate. Though not all buildings will be suitable for conversions, the largest cities with an abundance of obsolete and/or commodity office product are likely to see the most activity.

- According to Green Street Advisors, pricing declined 9.0% quarter-over-quarter. Further erosion of asset values is likely, as the market absorbs capital markets

uncertainty, further FOMC hikes and price discovery. Additionally, cap rate expansion is highly likely in the coming quarters. While NCREIF total returns remain positive, returns have decelerated swiftly in the third quarter of 2022 and likely could see further erosion, like multifamily REITs have experienced.

The Economy Is Not in a Recession (Yet)

Consumer spending is still above the pre-pandemic trend, though the rate of growth is rapidly decelerating.

The Economy Is Not in a Recession (Yet)

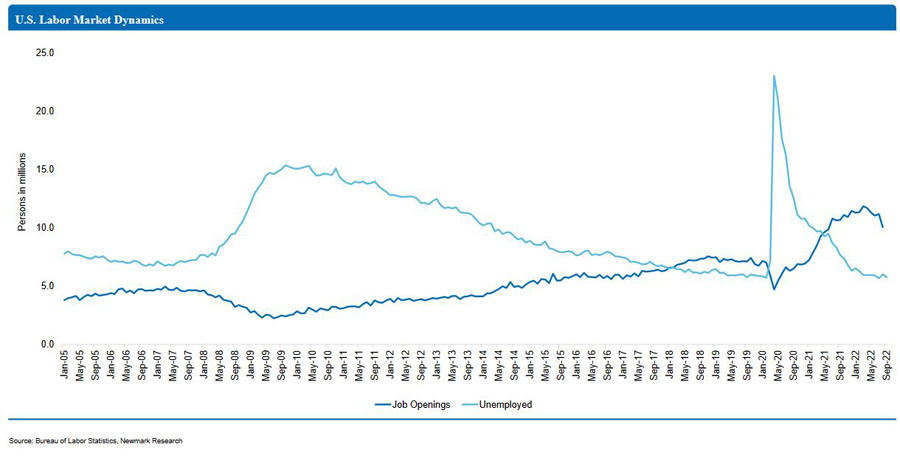

Jobs aren’t scarce, but labor is. There are 1.7 open positions for every unemployed worker.

To read the full report click here.