Phoenix 4Q Retail Performance Breaks Records

Vacancy and Absorption Overall Phoenix

Vacancy and Absorption Overall Phoenix

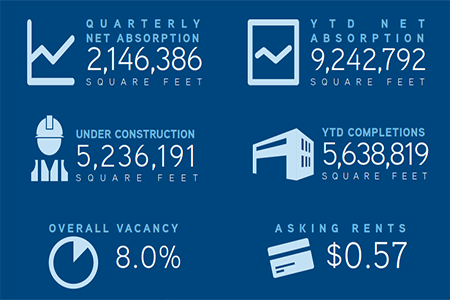

The retail market in the Phoenix metro area has improved every year for the past six years. Slow and steady improvement each year has been recorded providing a bright future for retailers, building owners and investors looking at the Phoenix market.

Since 2012 the vacancy rate in Phoenix has improved 300 bps, with the current vacancy at 8.8%. Absorption is also strong with 2.25 million square feet leased in 2017. These indicators, combined with healthy new construction deliveries of 1.7 million square feet make for a trifecta of positive indicators in commercial retail for Phoenix.

In looking ahead to 2018, we project continued steady absorption, new construction that is fueled by tenant demand, and a continued decrease in the vacancy rate.

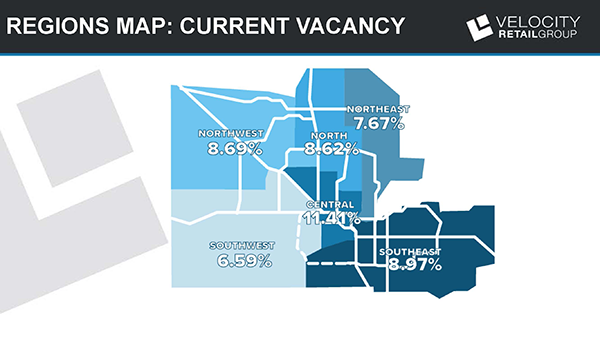

The Phoenix Regional Submarkets

Our research breaks the Metropolitan Phoenix area into six regional submarkets.

During 2017 the Southeast Valley recorded the greatest improvement and is an “All Star” performer in our books.

The Southeast Valley was one of the hardest hit submarkets during the recession. In 2012 the area had a 13.4% vacancy rate. Fast forward to 2017, currently the area has a vacancy rate of 8.9%, which is a 450 bps improvement. During 2017 the Southeast Valley also recorded the greatest amount of absorption, totaling nearly 1.3 million square feet. This was over 57% of the absorption for the entire Phoenix metro market. No other region came close to recording this amount of absorption. The Southeast region also captured the greatest amount of new construction activity during 2017, with over 38% of the new space built being within this regions boundary’s.

Another Regional All Star is the Southwest Valley, with a current vacancy rate of 6.6% this is the submarket with the lowest recorded vacancy. In 2012 the vacancy rate was 9.9%, which is a 330 bps improvement in this time period. Absorption totaled just over 200,000 square feet, with new construction projects at 208,000 square feet.

Overall, each of the six submarkets improved in vacancy and absorption year over year. With continued strong retailer demand we expect continued progress on all fronts across the Valley.