Tucson MSA Multifamily 2Q 2017 Quarterly Report

By: Thomas M. Brophy, Director of Research, ABI Mulitfamily

By: Thomas M. Brophy, Director of Research, ABI Mulitfamily

TUCSON, Arizona — The MSA’s total sales volume (10+ unit properties) increased 167%, year-over-year, to $168.95M across 44 transactions representing 2,263 total units sold. California-based investors continue to be the dominant buyer of multifamily properties in the area accounting for 34% of total units transacted or 772 units, Arizona-based investors came in 2nd with 540 units purchased and, rounding out the top five: (#3) Florida-investors with 455 units purchase, (#4) Massachusetts-based investors with 274 units and (#5) Nevada-based investors with 141 units.

Sales of 100+ unit properties witnessed a sales volume increase of 117% y-o-y to $95.9M. Average price-per-unit amount increased 25% to $81,122. 10 to 99 unit properties saw its volume increase an astounding 283% to $72.9M with a surge of 101% in average price-per-unit amounts to $67,578. Price-per-unit increases in the smaller property size category dovetails the sales trend which began in earnest in late 2016 through 1Q 2017, as mid-century built, extensively repositioned properties in the Central Tucson/University submarket having been coming back online for sale. In fact, pre-1980’s built product represented 74% of all transactions in the 2Q.

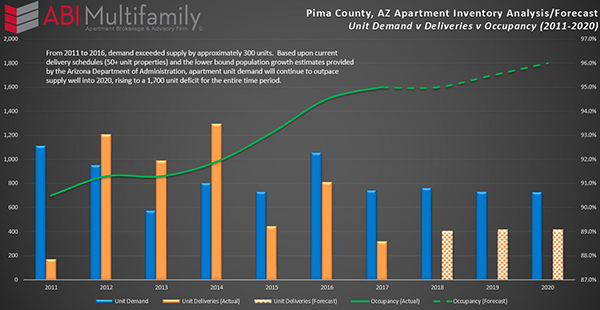

The Tucson MSA did not have any new inventory come online in 2Q. In fact, Tucson will not see any new construction until the end of 2018, aside from smaller affordable housing developments. Despite a minor (0.2%) Occupancy Rate contraction to 94.4%, Tucson’s Occupancy Rate is projected to increase to 95% by year end. Average rent continued is rise increasing 3.8% y-o-y to $794.

Outlook I firmly stick behind my 2017 Market Forecast, despite Fed chatter and three 25-50bps increases behind us, it is unlikely the Fed will continue with its gradual interest rate increase for the balance of 2017 despite many economists predicting otherwise. Basis for this sentiment is rooted in two primary areas, namely weak inflationary pressures, as stated by Yellen, and continued sub-3% GDP growth post-recession. This isn’t to say that we are without headwinds; in fact, given government stasis in key legislative areas, specifically healthcare and tax reform, has resulted in loss of the ‘Trump bounce’ yet people remain largely optimistic. Additionally, despite the projected end to gradual interest rate increases, the Fed has made statements it wants to move towards ‘balance sheet reduction’ or QT, quantitative tightening, which certainly has the potential to sap liquidity from the market. Internationally there is still significant instability in both EM (Emerging) and DM (Developed) markets, particularly across Europe and Asia. It’s helpful to remember some 50%+ of the world’s developed markets continue to operate at zero or below interest rates which has led to capital flight. Despite stocks hitting all-time highs, based in large part on investors factoring in massive deregulation, markets the world over have been prone to ever increasing volatility fits.

With many of the larger western MSA’s reaching, and exceeding, previous peak price per unit amounts has caused investors, on the hunt for higher yield/CAP rates, to look to qualified secondary and tertiary markets. Tucson with little in the development pipeline, is fast becoming the ‘go-to’ secondary market for multifamily investors. Given Tucson’s now 5-year low for projected new unit deliveries and with economic and job prospects at, or nearing, 7 year highs lays the foundation for a market not witnessed by Tucson investors in at least a generation, if ever. The confluence of these two conditions will continue to shape the Tucson multifamily market well into the latter half of 2018 as new units will be brought online. Until that time both, and barring any Black Swan events, Occupancy Rates and Rents should continue to reach all-time highs and make Tucson one of the more active secondary markets in the country.

For full report click here: ABInsight-Tucson-MSA-2Q-2017-Review-Construction-Glut-to-Intensify-Investor-Demand