![]() U.S. office leasing increased by 27% in 2021, with technology companies driving demand for the largest requirements. While the 100 largest leases’ share of total U.S. office leasing dropped to 15.5% last year from 19% in 2020, their total square footage increased by 6.8% to 31 million.

U.S. office leasing increased by 27% in 2021, with technology companies driving demand for the largest requirements. While the 100 largest leases’ share of total U.S. office leasing dropped to 15.5% last year from 19% in 2020, their total square footage increased by 6.8% to 31 million.

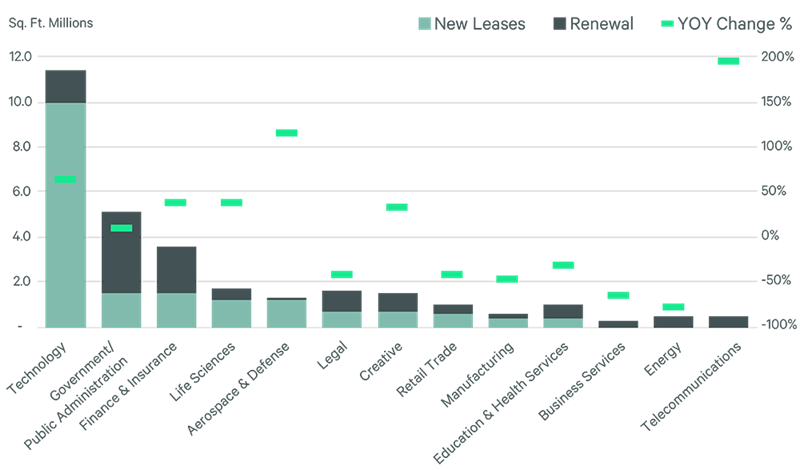

New leases accounted for 61% of the top 100, up from 57% in 2020, as companies became more comfortable with making long-term occupancy decisions.

Technology companies accounted for 36 of the top 100 leases, double their share in 2020, for 11.4 million sq. ft. or 37% of the top 100 total. On a square footage basis, 87% of the technology company total was in new leases or expansions, reflecting the sector’s uninterrupted growth during the pandemic. The aerospace/defense and life sciences sectors also had relatively high numbers of new leases.

The government/public administration sector accounted for 16 of the top 100 leases, totaling 5.1 million sq. ft. Most of those commitments (70%) were renewals and were primarily in Washington, D.C.

The average size of the top 100 leases rose by 7% year-over-year to 307,000 sq. ft. Nine of the 13 industry sectors tracked by CBRE Research recorded increases in the average size of their largest leases. The creative, aerospace/defense and telecommunications sectors posted the largest increases. The energy sector had the largest decrease (-50%), followed by retail (-27%) and technology (-16%).

FIGURE 1: 2021 Top 100 Office Leases by Industry Sector Share

Source: CBRE Research, February 2022.

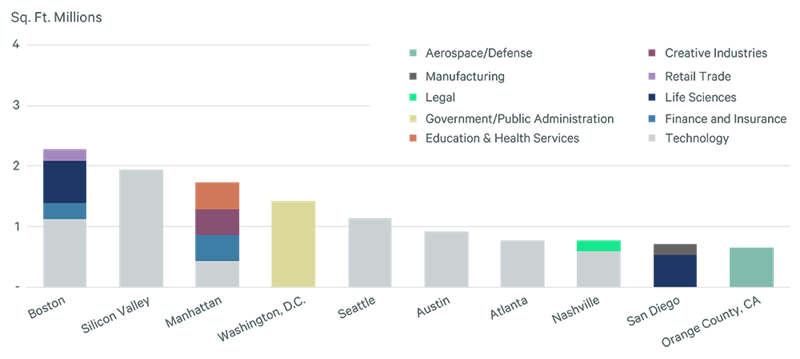

Manhattan, Washington, D.C. and Boston were the top three markets for total top 100 leasing volume (35%), including renewals, primarily driven by the finance/insurance, government/public administration and technology sectors, respectively. Of the total top 100 in these three markets, 49% was in new leases.

Boston, Silicon Valley and Manhattan were the top three markets for new leasing activity among the top 100 (Figure 2).

FIGURE 2: Top 100 New Lease Totals by Leading Markets & Industry Sector

Source: CBRE Research, February 2022.

Occupiers continue to evaluate the most efficient ways to utilize office space. The recent growth in office-using employment and the slowdown of the COVID omicron variant should embolden more occupiers to make long-term decisions. The increased leasing activity in the second half of 2021 is expected to continue in 2022.