By: Thomas M. Brophy, Director of Research, ABI Multifamily

Do Negative Interest Rates Abroad Impact Domestic Commercial Real Estate? In Arizona?

In NIRP We Trust

As I sit down to type this post much in the world of economics and markets has occurred; first, the Nation’s August jobs data was released. As referenced on the chart/table below, most of the job/wage growth came from the lower-tier (Bottom 20%) of the job spectrum.

According to Elliott D. Pollack & Company, Arizona, during the first 7 months of 2016, continued to see robust employment growth up 3% to date. In fact, both the Phoenix and Tucson Metro’s outpaced most of the country with robust employment growth 3.4% (or 58,000 jobs since July 2015) and 3.3% (or 14,900 jobs since July 2015) respectively over the same time period. The largest job category gains were seen in the information, financial activities, educational and health services and manufacturing sectors.

According to Elliott D. Pollack & Company, Arizona, during the first 7 months of 2016, continued to see robust employment growth up 3% to date. In fact, both the Phoenix and Tucson Metro’s outpaced most of the country with robust employment growth 3.4% (or 58,000 jobs since July 2015) and 3.3% (or 14,900 jobs since July 2015) respectively over the same time period. The largest job category gains were seen in the information, financial activities, educational and health services and manufacturing sectors.

Second, Fed Chairwoman, Janet Yellen, gave her highly anticipated, albeit underwhelming, Jackson Hole speech. As Janus Capital’s, Bill Gross, points out, “With Yellen, there is no right or left hand — no “on the one hand but then on the other” – there are only decades of old orthodoxy that follows the tarnished golden rule of lowering interest rates to elevate asset prices, which in turn could (should) trickle down to the real economy.”

Third, the ECB (European Central Bank) confirmed its continued commitment to negative interest rates of (0.4%) on deposits and left its benchmark main refinancing rate at 0%. Additionally, the ECB will continue its massive QE schedule of €80 billion in monthly asset purchases through March 2017 and beyond. Mike Shedlock, SitkaPacific Capital Management, in his blog, MishTalk, summed up the ECB’s failed monetary policy in one chart (shown below):

Last but not least, both the stock and bond markets have experienced tremendous volatility resulting in investor whiplash. Although the DOW, NASDAQ and S&P are still up for 2016 (as of 9/13/16) at 3.68%, 2.95% and 4.06% respectively, they’ve seen an average reduction of 1.33% in the last few days of trading alone. The sum total of the Jackson Hole meet, stated ECB monetary policies, continued Abenomics in Japan, lackluster US growth and continued market volatility all points to very little chance of a US interest rate increase for the rest of this year, despite some Fed official’s hawkish comments otherwise. In light of the Fed’s focus on NIRP at Jackson Hole, particularly Marvin Goodfriend (Carnegie Mellon University) and Marianne Nessen’s (Swedish Central Bank) in defense of NIRP (and more negative rates) speeches, I’d say we’re all but guaranteed no interest rate increases for, at least, the next few quarters.

Last but not least, both the stock and bond markets have experienced tremendous volatility resulting in investor whiplash. Although the DOW, NASDAQ and S&P are still up for 2016 (as of 9/13/16) at 3.68%, 2.95% and 4.06% respectively, they’ve seen an average reduction of 1.33% in the last few days of trading alone. The sum total of the Jackson Hole meet, stated ECB monetary policies, continued Abenomics in Japan, lackluster US growth and continued market volatility all points to very little chance of a US interest rate increase for the rest of this year, despite some Fed official’s hawkish comments otherwise. In light of the Fed’s focus on NIRP at Jackson Hole, particularly Marvin Goodfriend (Carnegie Mellon University) and Marianne Nessen’s (Swedish Central Bank) in defense of NIRP (and more negative rates) speeches, I’d say we’re all but guaranteed no interest rate increases for, at least, the next few quarters.

Got Yield? The Capital That Moves Markets

As I stated in my 2016 Market Forecast back in January, Congress passed a provision in its December 2015 $1.1 trillion spending bill modifying the 1980 Foreign Investment in Real Property Tax (FIRPTA). To recap:

“FIRPTA has historically made direct investment in U.S. property a non-starter for trillions of dollars-worth of foreign pensions,” said James Corl, a managing director at private equity firm Siguler Guff & Co. “This tax-law modification is a game changer” that could result in hundreds of billions of new capital flows into U.S. real estate….The new law also allows foreign pensions to buy as much as 10 percent of a U.S. publicly traded real estate investment trust without triggering FIRPTA liability, up from 5 percent previously….Cross-border investment in U.S. real estate has totaled about $78.4 billion this year, or 16 percent of the total $483 billion investment in U.S. property, according to Real Capital Analytics Inc. Pension funds accounted for about $7.5 billion, or almost 10 percent, of the foreign total, according to the New York-based property research firm.

Professional researchers, such as myself, and economists are (or should be) obsessed with the impact of marginal, or outlier, moves in a given market. The reason marginal/outlier moves impact markets is that they can, but not always, exacerbate and distort normal market pricing conditions, which one could postulate is already distorted due to our decade old Fed-induced Zero Interest Rate Policy (ZIRP).

For example, I’ve been particularly interested in following the capital that has come from Europe, specifically Germany where NIRP policies have pushed banks to charge fees for nominal deposits (€111,000 or more), to US (Arizona) commercial real estate. Specifically, is there a price per unit premium paid by foreign investors fleeing the draconian impacts of NIRP policies? Although our more detailed analysis is for clients only, suffice-it-to-say that in late 2015 the Phoenix Metro began seeing a noticeable increase in German investment capital targeting multifamily properties in the Tempe and Chandler submarkets. As GlobeSt recently reported, North Carolina-based Bell Partners and Hamburg, Germany-based Hanseatische Investment-GmbH have partnered in the creation of a multifamily investment fund. The new investment fund has a $1 billion, $500 million of equity, cap and is targeting core multifamily properties in metro areas with strong fundamentals. As NIRP policies continue to distort investor sentiment (especially acute in European markets), I would not be surprised to see ever increasing amounts of foreign money pushing the sales price per unit margins higher in the coming months and into next year.

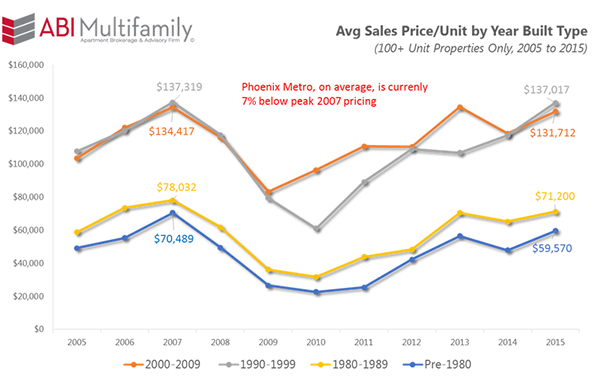

Despite Significant Price Increases, Phoenix is still below Peak Pricing

Whereas many markets across the US have exceeded peak sales price per unit amounts, Phoenix Metro, despite our frenetic sales pace, is still an average of 7% below our 2007 peak (see chart below):

As shown in our Phoenix Metro per City Analysis: Rents, Occupancy, Population & Affordability post, despite sustained average per year rental rate increases of approximately 4%+, elevated construction amounts (although nowhere near peak building), the Phoenix Metro is at historical highs both in terms of occupancy, trending towards 97%, and renter retention, which at nearly 55% is some 3% higher than the national average.

Conclusion

Whether or not one agrees with current Central Banker NIRP (or ZIRP) policy, truly matters not, as it is the market in which we must play. Considering Fed governor posturing, and although there are those who disagree, I anticipate stasis of domestic interest rates and further dives into deeper negative rates for most of Europe which has the potential to set off massive capital flights to preservation as opposed to yield. In Phoenix, we’re already experiencing some of that premium pricing setting in, however is not as extreme as those markets on the East/West coasts. As such, I would expect both the Phoenix and Tucson markets to continue their upward trends through the end of the year and well into next.

For full article Click Here.