(June 10, 2026) — The national labor market showed renewed strength in May, offering a positive signal for commercial real estate demand even as employers continue to navigate labor constraints, higher operating costs, and uncertainty over interest rates.

According to Marcus & Millichap’s June 2026 Employment Research Brief, employers added 176,000 jobs in May, while upward revisions to March and April added another 91,000 positions. The unemployment rate held steady at 4.3 percent, continuing a narrow range that has remained relatively stable since mid-2025.

For commercial real estate, the takeaway is straightforward: job growth continues to support household formation, consumer spending, and demand for space. That is especially important for multifamily, retail, and service-oriented real estate, where employment gains help sustain rental demand and local spending.

Hiring was also broader than in recent months. Marcus & Millichap reported that 10 of 14 major employment sectors added jobs in May, led by leisure and hospitality, local government, health care, and construction. Those are categories that matter directly to real estate markets because they influence apartment demand, retail sales, medical office activity, construction pipelines, and local tax bases.

The report also noted that the U.S. economy appears less vulnerable to energy shocks than it was in previous decades. While conflict in the Middle East and uncertainty around the Strait of Hormuz remain concerns, Marcus & Millichap pointed to reduced dependence on oil imports, lower oil intensity, and a more service-driven economy as factors that help limit the employment impact. That resilience is important for real estate investors watching fuel prices, transportation costs, and consumer confidence.

For Southern Arizona, the national picture is encouraging but also highlights the region’s own challenge: Tucson needs more private-sector job growth to fully benefit from the broader economic momentum.

Recent local employment data showed Tucson adding jobs month over month in April, but much of that gain came from government employment. The metro area remained slightly below its year-earlier employment level, while Phoenix continued to post stronger year-over-year job growth. That contrast reinforces a familiar economic development message for Southern Arizona: the region has assets, affordability, and capacity, but it must continue competing for primary employers, higher-wage industries, and private-sector investment.

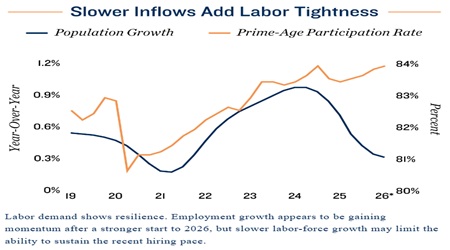

Marcus & Millichap’s report also pointed to labor-force limits as a constraint on future growth. Prime-age employment remains elevated, with the 25- to 54-year-old employment-population ratio near 81 percent, above its post-2000 average. Participation among that core working-age group is also high, meaning much of the available labor pool is already engaged.

That could create what the report describes as a “low-hire, low-fire” environment, where employers focus more on retaining workers than aggressively expanding payrolls. For multifamily owners, this may support resident retention and renewal rates. Marcus & Millichap reported renewal conversions near 57 percent in April, while new lease terms remained close to record highs.

The office-using employment picture remains more complicated. Artificial intelligence was cited in a growing share of job cuts, and information and financial activities posted losses. However, Marcus & Millichap noted that software engineering openings were up year over year, while professional and business services openings surged to their highest level since 2023. The implication is not that office demand has disappeared, but that office-using employment is shifting.

That matters for Tucson as the region works to strengthen its technology, defense, aerospace, bioscience, and professional services sectors. Office demand is unlikely to return in the same form seen before the pandemic, but employers that need specialized talent, collaboration space, and proximity to research institutions can still support targeted demand in well-positioned locations.

Wage growth also remained moderate. Average hourly earnings increased 0.3 percent month over month and 3.4 percent year over year in May. Marcus & Millichap said that steady income growth should help support consumer spending, while the pace of wage gains may limit additional inflation pressure.

For investors, developers, and economic development leaders, the May employment data offers a cautiously positive message. The economy is still creating jobs, consumers still have income support, and several property sectors continue to benefit from employment stability. At the same time, labor-force constraints, slower population growth, elevated interest rates, and uneven regional job creation remain important risks.

In Southern Arizona, the report underscores why private-sector job growth remains central to the region’s real estate outlook. More jobs support more households, stronger retail spending, healthier apartment absorption, and greater demand for commercial space. But the type of job growth matters. Government hiring can stabilize a market, but primary employers and higher-wage industries are what expand the economic base.

The national labor market may be entering a firmer phase. The opportunity for Tucson is to make sure Southern Arizona is positioned to capture more of that momentum.