PIMA COUNTY (March 8, 2024) Property owners throughout Pima County are now receiving their Notices of Value for Tax Year 2025. These notifications, sent out on Feb. 28, provide crucial information about property assessments for taxation purposes and are expected to reach taxpayers throughout the course of the week.

PIMA COUNTY (March 8, 2024) Property owners throughout Pima County are now receiving their Notices of Value for Tax Year 2025. These notifications, sent out on Feb. 28, provide crucial information about property assessments for taxation purposes and are expected to reach taxpayers throughout the course of the week.

The Assessor’s Office undertakes the monumental task of annually discovering, listing, and valuing all taxable property in Pima County including residential and commercial property, business equipment, as well as vacant and agricultural land. A primary objective of the Assessor’s Office is to safeguard the county’s tax base by adding new and improved properties to the tax roll each year while working directly with county taxpayers to apply any relevant exemptions to their property assessments. By law, the Assessor’s Office is responsible for notifying property owners of their assessed value - these notifications serve as essential documents for property owners, providing key information such as the Full Cash Value (FCV), Limited Property Value (LPV), and the property classification.

Late last week, the Assessor’s Office issued a total of 424,188 notices to taxpayers across Pima County. The total Full Cash Value (FCV) of all real property in Pima County rose to approximately $156 billion for Tax Year 2025, reflecting a 4.3% increase over the 2024 value of $149.5 billion.

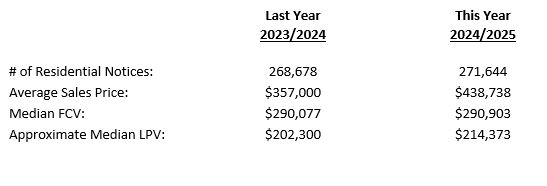

The majority of notices issued by our office pertained to single-family residential properties in Pima County. The below comparison provides insights into changes in the number of notices issued, average sales prices, median full cash values, and approximate median limited property values for residential properties within the county.

Suzanne Droubie, Pima County's Assessor, recently contributed the following information on Understanding Property Valuation and the Appeal Process in Pima County to the March issue of Trend Report. We are reprinting it here for all property owners in Pima County.

The Pima County Assessor’s Office undertakes the monumental task of annually discovering, listing, and valuing over 424,188 real property parcels throughout Pima County. Safeguarding the county’s tax base is a primary focus of the Assessor’s Office, which is achieved by adding new and improved properties to the tax roll each year. In line with this commitment, the Pima County Assessor’s Office mailed the Tax Year 2025 Notice of Value on February 28, 2024. These notices serve as essential documents for property owners, providing key information such as the Full Cash Value (FCV), Limited Property Value (LPV), and the property classification.

The Notice of Value allows property owners to dispute their property assessment should they disagree with the valuation or classification assigned by the County Assessor. Within 60 days of the mailing date, property owners may petition the Assessor’s Office for review, supported by clear and well-defined rights of appeal. Property owners may pursue appeals through two distinct avenues, affording taxpayers with the flexibility in seeking recourse against assessments they feel are improperly valued or erroneously listed:

- Administrative Appeal: Property owners can initiate an administrative appeal by filing petitions directly with the Assessor or the State Board of Equalization. This free process allows for a formal review of the assessment without the need for court involvement.

- Judicial Appeal: Alternatively, property owners can pursue a judicial appeal by filing their property appeal directly with the court. These appeals are managed within the legal system, often involving formalized court proceedings for an associated fe

Understanding Property Valuation

Property values in Pima County are determined using a comprehensive approach that considers various data and property factors. There are three methods of appraising or establishing the Full Cash Value (FCV) of a property:

- Replacement Cost New Less Depreciation: The cost of reproducing or replacing a property, plus land value, minus the accrued depreciation.

- Market/Sales Comparison Approach: The value indicated by recent sales of comparable properties in the market, with adjustments for age, condition, and other characteristics.

- Income Approach: The investment value represented by the net earning power of a property based on the capitalizing income stream it generates.

Each method is applicable in different scenarios based on property type and characteristics. For example, owner-occupied residential properties typically do not generate rental income that could be capitalized into an estimate of value using the income approach. In such cases, the sales comparison or cost approach might be more suitable. Similarly, vacant land does not include the cost of improvements, rendering the cost approach unsuitable in this scenario. Specialized properties, such as mortuaries, hospitals, or zoos often have limited sales data for comparison,

making the cost or income approach more appropriate. By understanding the unique circumstances of each property, our appraisers can determine which valuation method to apply to ensure fair and accurate assessments for our constituents.

Getting Started

At the Assessor’s Office, we are dedicated to ensuring fairness, equity, and accuracy in our property valuations. If you are a property owner who disagrees with the assessed value of your property, we are committed to assisting you through the appeals process.

- Review Your Listing: Examine the characteristics of your property and identify any errors or omissions you feel impact the value of your property. Verify your property classification for accuracy.

- Assess Market Activity & Established Market Values: When filing an appeal, you must state the method or valuation methods you base your appeal • If the petition is based on the Market Approach, you must include the sale price of at least one comparable property in the same geographic area or the sale of the subject property.

• If the petition is based on the Replacement Cost Approach, it must include the average cost to rebuild the property by a contractor or accepted professional, plus the land value.

• If the petition is based on the Income Approach, it should include information as required by A.R.S. § 42-16052. - Prepare Your Appeal: Your appeal will have a greater chance of success when you can prove at least one of the following:

• Your property record may contain inaccuracies such as misrepresented square footage, construction year, garage, or carport details.

• The Full Cash Value (FCV) is disproportionately high compared to similar properties in your neighborhood or recent sales within the last 3 years. It is possible that your purchase price was lower than the Full Cash Value (FCV). In this event, please get in touch with our office to discuss the guidelines regarding sales to be considered in this case (i.e. Arm’s-Length Transactions, not under Duress, etc.).

• If the income-generating potential of your property suggests that the estimated market value is excessively high, it warrants further examination.

• There may be instances where the Limited Property Value has been calculated incorrectly, warranting a review of the assessment.

• Inaccurate listing of the property’s classification can also impact the assessment. We advise allproperty owners to carefully review their annual Notice of Value to ensure they are listed under the correct property classification.

For residential properties, the Assessor’s Office offers access to the comparable sales utilized in determining your assessed value. Sales and equity comparables are readily available on your property’s parcel detail page on the Assessor’s website. For a more comprehensive list of values throughout Pima County, both commercial and residential, please call our office.

Preparing Your Appeal

To ensure a seamless appeal process, we ask that you please be mindful of the statutory deadlines that protect the rights of both property owners and the taxing authorities. By adhering to these deadlines, property owners ensure they have ample opportunity to dispute their property assessments in a timely manner, while the Assessor’s office maintains an orderly appeals process for our staff and our constituents.

Step 1: Appeals to the Assessor

Petitions filed with the county Assessor in the county in which the property is located must be filed within sixty (60) days of the date postmarked on the Notice of Valuation.

A completed Petition for Review of Valuation form may be completed online (residential), mailed, or hand delivered to the Assessor’s Office. Please retain a copy for your records for use in possible further appeals.

Step 2: Appeals to the State Board of Equalization

If you are not satisfied with the Assessor’s decision, you may file a petition with the State Board of Equalization within 25 calendar days after the Assessor’s decision is mailed.

A copy of the original notice of valuation, the completed agency authorization form (if applicable), the petition, and the Assessor’s decision should be submitted to the State Board of Equalization. Guidelines and filing requirements are found on the Arizona State Board of Equalization website.

Step 3: Appeals to Tax Court

Suppose you have filed an appeal through the administrative process and/or are dissatisfied with the valuation or classification of your property as determined by the County Board of Equalization. In that case, you may submit your appeal to the Tax Court within sixty (60) days of the mailing date of the most recent administrative decision. If you have not started the administrative process, you may appeal directly to the Tax Court on or before December 15th for the notice value sent in that year.

As the Pima County Assessor, I am dedicated to ensuring fairness, equity, and transparency for all county taxpayers, alongside delivering the exceptional customer service our constituents have come to rely on. However, my commitment extends far beyond providing fair and equitable property assessments. My team supports our constituents through this process, providing a successful appeal season for our property owners, tax agents, and staff. While errors and discrepancies may arise, we encourage property owners across Pima County to contact our office. Our goal is not to “be right,” but to “get it right” as we strive to maintain the public’s trust in our valuations and services.

Thank you for entrusting us with this task. Moving forward to a new fiscal year, we remain committed to “putting the service BACK in Public Service.”

Suzanne Droubie was elected as the first female Assessor of Pima County in 2020. With over 26 years of combined experience as a taxpayer consultant, mass appraiser, fee appraiser, litigation expert, and real estate specialist, Assessor Droubie brings a wealth of expertise and leadership skills. Her unwavering commitment to providing exceptional customer service has transformed the Assessor’s Office into a valuable resource for the constituents of Pima County. Beyond her accomplishments in the public sector, Suzanne held the esteemed position of Vice President of Property Tax Services for a national Fortune 100 company, advising colleagues, associates, and clients on all aspects of commercial property tax. Continuously fulfilling her statutory obligations, Assessor Droubie remains dedicated to transparency, fairness, and equity for all county taxpayers. Beyond her statutory duties, she has implemented innovative programs and services that propel the Assessor’s Office towards a more efficient and sustainable future. Her forward-thinking approach reinforces her commitment to serving the community and advancing the overall effectiveness of the Pima County Assessor’s Office.

Suzanne Droubie was elected as the first female Assessor of Pima County in 2020. With over 26 years of combined experience as a taxpayer consultant, mass appraiser, fee appraiser, litigation expert, and real estate specialist, Assessor Droubie brings a wealth of expertise and leadership skills. Her unwavering commitment to providing exceptional customer service has transformed the Assessor’s Office into a valuable resource for the constituents of Pima County. Beyond her accomplishments in the public sector, Suzanne held the esteemed position of Vice President of Property Tax Services for a national Fortune 100 company, advising colleagues, associates, and clients on all aspects of commercial property tax. Continuously fulfilling her statutory obligations, Assessor Droubie remains dedicated to transparency, fairness, and equity for all county taxpayers. Beyond her statutory duties, she has implemented innovative programs and services that propel the Assessor’s Office towards a more efficient and sustainable future. Her forward-thinking approach reinforces her commitment to serving the community and advancing the overall effectiveness of the Pima County Assessor’s Office.