Tuesday, CoreLogic reported that July 2014 national home prices increased by 7.4% year-over-year, and by 1.2% month-over-month. This marks the 29th consecutive month of year-over-year increases in the CoreLogic Home Price Index (HPI). Excluding distressed sales, home prices increased 6.8 % from July 2013 and were up 1.1% from the prior month. Including distressed sales, prices were still 11.9% below the peak in April 2006, and excluding distressed sales, prices were down 8.3% from peak levels.

Including distressed sales, year-over-year home prices were up in every state but Arkansas. Michigan led the country with an 11.4% price increase from July 2013, followed by Maine with a 10.6% increase. Excluding distressed sales, all states experienced a year-over-year rise in prices, with Massachusetts (+11.2%) and New York (+9.7%) showing the largest increases.

Twelve states reached new highs in home prices in June 2014, were: Texas, Colorado, North Dakota, Tennessee, South Dakota, District of Columbia, Vermont, Alaska, Nebraska, Oklahoma, Louisiana, and Iowa.

In addition to the overall price indices, CoreLogic analyzes four individual home-price tiers. The price tiers tracked by the CoreLogic HPI are calculated relative to the mean national home price and include homes that are priced 75 % or less below the mean (low price), between 75 and 100 % of the mean (low-to-middle price), between 100 and 125% of the mean (middle-to-moderate price) and greater than 125% of the mean (high price).

Figure 1 shows the levels of the four price tiers indexed to January 2011. The two lower-priced tiers have recovered the most from their trough levels (both hit bottom in March 2011), with the low-price tier recovering 41% from the trough and the low-to-middle tier recovering 35.3 % from the trough. As of July 2014, the low-price tier increased 11.1% year-over-year. The two higher-price tiers both bottomed out in February 2012, with the middle-to-moderate price tier recovering 32.5% from the trough and the high-price tier recovering 27.1% from the trough. The high-price tier fell the least, at 27.9% peak-to-trough, and is currently 8.4% below its peak. The low-to-middle price tier fared the worst in the housing crisis, falling 37.2% peak-to-trough, and is now 15% below peak levels.

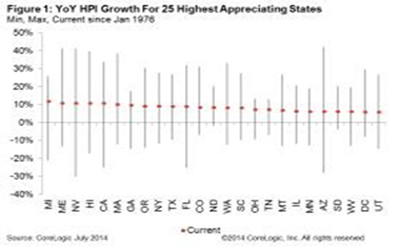

Figure 2 shows the current, maximum and minimum year-over-year growth rates for the 25 states with the highest year-over-year appreciation. The figure illustrates that some of the states now growing the fastest also fell the farthest in the housing crisis. The five states with the largest peak-to-current declines, including distressed transactions, were: Nevada (-36.4%), Florida (-33.0%), Arizona (-28.9%), Rhode Island (-26.9%) and New Jersey (-20.6%).