New NAHB 2022 Priced-Out Estimates showed that 87.5 million households are not able to afford a median priced new home, and that additional 117,932 households would be priced out of the new home market if the price goes up by $1,000. This post presents how interest rates affect the number of households that would be priced out of the new home market.

New NAHB 2022 Priced-Out Estimates showed that 87.5 million households are not able to afford a median priced new home, and that additional 117,932 households would be priced out of the new home market if the price goes up by $1,000. This post presents how interest rates affect the number of households that would be priced out of the new home market.

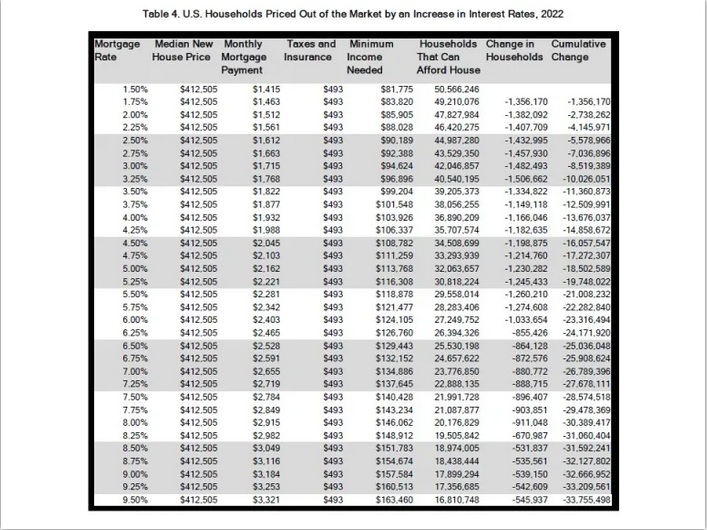

For a new home with an estimated median price of $412,506 in 2022 and the recent 30-year fixed-rate mortgage rate of 3.5%, a quarter percentage point increase in the interest rate would price out approximately 1.1 million households. The monthly mortgage payments will increase as a result of rising mortgage interest rates, and therefore higher household income thresholds would be needed to qualify for a mortgage loan.

The table below shows the number of households priced out of the market for a new median priced home at $412,505 by each 25 basis-point increase in interest rates from 1.5% to 9.5%. When interest rates go up from 1.75% to 2.00%, around 1.4 million households could no longer afford buying median-priced new homes. An increase from 3.5% to 3.75% could price approximately 1.1 million households out of the market. However, at considerably higher rates this number tapers. For example, increasing from 6.25% to 6.5% mortgage rates prices out 0.86 million households. This diminishing effect happen because only a declining number households at the higher end of household income distribution will be affected. On the contrary, when interest rates are relatively low, a 25 basis-point increase would affect a larger number of households at the lower and more populous part of income distribution.